Market volatility and economic uncertainty have dominated the last six months, which caused a strong correction in capital markets. In the midst of these challenges, low volatility, mutual funds based on factors have demonstrated resilience, which contains more effective losses than the index of parents and other factors based on factors.

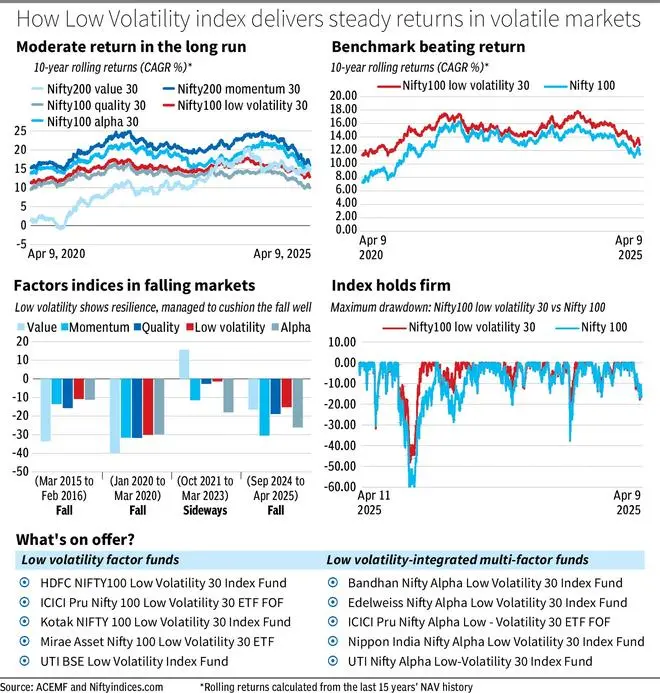

The NIFTY100 Low Volatility 30 decreased 15.1 percent in its September 2024, while its main NIFTY 100 index fell slightly more to 15.7 percent. On the contrary, other factors indices saw deeper cuts: NIFTY200 MOMENTUM 30 (-31 percent), NIFTY100 ALFA 30 (-26 percent), Quality NIFTY 30 (-19 percent) and NIFTY200 (-16.5 percent) value. The total return index (TRI) is a consultant.

Considering its strong performance in volatile markets, should investors assign funds based on low volatility factors? These effective strategies limit the downward risk, but their performance delays the duration of the trend bundle markets. We explore the fundamental characteristics of this strategy and compare it with other factors -based approaches.

Cyclic nature

Low volatility is one of several intelligent beta investment strategies designed to overcome indexes based on traditional market capitalization under specific market conditions. Beta intelligent funds passively track the indices that are derived from the conventional reference points using various fundamental, technical and other filters applied by NSE and BSE. The NIFTY 100 index Volatility 30 repeats 30 NIFTY 100 actions that have demonstrated the lowest volatility during the past year.

Other factors widely used in intelligent beta investment include quality, value, impulse and alpha. The performance of intelligent beta strategies tends to be cyclical: some periods see strong yields, while others bring low performance. Low volatility tends to overcome at the gates of uncertain or turbulent markets. On the contrary, value strategies often shine in the recovery phases of duration, quality works well in volatile or bassist markets, and the impulse tends to lead in the trend bundle markets strongly.

Low volatility portfolios are built according to price performance, specifically by evaluating the standard deviation of daily prices yields in the last year. Currently, 11 mutual fund schemes used the low volatility strategy. Of these, nine track the NIFTY 100 Volatility 30 Index, stocks of low selection volatility of the Nifty 100 Universe. The remaining two follow the BSE low volatility index, which selects 30 actions of low volatility of a broader group of 250 large and medium companies. In addition, five mutual fund schemes incorporate low volatility as part of a multifactor approach.

Defensive portfolio

Low volatility portfolios generally include companies with stable businesses. These wallets tend to move away from highly cyclical or speculative stocks, instead of leaning towards defensive sectors, such as basic consumption products, public services and medical care. In the last five years, the main sectors (as classified by the ACEMF database) that were part of the NIFTY 100 Index.

These portfolios generally avoid sectors prone to volatile gains and shares prices, such as real estate products, real estate, capital goods and cyclic discretionary segments of the consumer as luxury goods. Among the best actions that have constantly appeared in the index with significant assignments are Nestlé India, Hindustan Unilever, Britannia Industries, Tata Consultancy Services and ITC.

Performance in several cycles

The low volatility strategy exhibits a distinctive performance behavior according to market conditions. It tends to work well in the rank markets. But its true strength becomes corrections of the market of apparent duration and bearish phases, where it generally experiences smaller decreases than the general market, which leads to remarkable relative performance. The attached table shows that the turn such as March 2015 to February 2016, January 2020 to March 2020, October 2021 to March 2023, and the ongoing phase, the low volatility index has effective losses.

However, this strategy tends to sit strong races of Toro, in large part because it avoids high beta stocks. Such a low performance is a compensation known for the protection it offers in recessions. Low volatility strategies generally trace the largest market duration marked by high -risk appetite, the economic rebounds that favor and the sector’s rotations towards growth and impulse issues.

Should you invest?

The inherently defensive nature of low volatility funds can lead to a slower growth in the portfolio over time. Limited exposure to average capitalization and avoidance of small capitalization can restrict a more upwards potential, especially compared to other factors -based strategies. However, the ability of the strategy to minimize the reduction of decrease positions these funds to offer more balanced returns and a long -term ultrasound ultrasound. The accompanying rolling return table shows that low volatility funds can generate constant and moderate yields on long -term horizons, such as 10 years or more. He published an annualized yield of 15 percent based on a continuous analysis of 10 years in the last 15 years.

For investors that prioritize stability and lower risk, especially uncertain market periods, these funds offer a convincing option.

Multifactor funds that incorporate low volatility in their approach can present an even better alternative. By combining multiple factors, they reduce dependence on a single strategy and are better equipped with performance consisting of different market cycles. At present, there are five of these schemes that combine alpha and low volatility available. A portfolio allocation of around 15-20 percent to these strategies could be a well-balanced option for investors with moderate risk profile.

Posted on April 12, 2025