The charts below are from Michael Mauboussin’s latest paper. I believe most UHNW individuals would benefit from having the chart below printed out for when venture deals come across their desks.

Over 31,000 observations of returns from global venture capital deals, covering the period from the mid-1990s to 2018, indicate that 62% of venture deals lose money, with more than half losing 50 to 100% of the invested capital. However, the potential rewards are significantly greater than those in public equities or buyouts, leading to fatter tails in the distribution of returns.

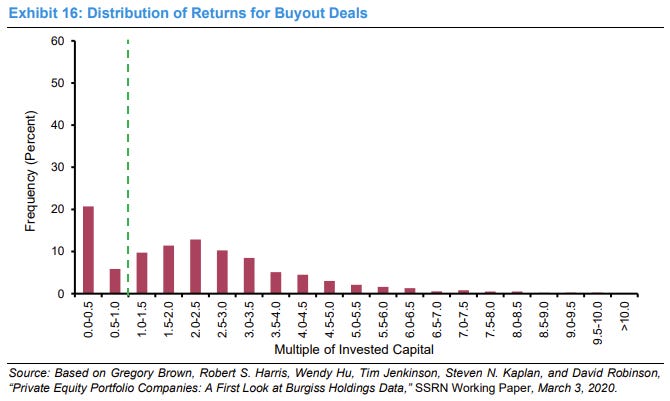

In over 15,000 observations of returns from global buyout deals, primarily conducted between the mid-1990s and 2018, 27% result in a loss. The most common outcome is a loss of 50 to 100 percent of the invested capital, with the distribution exhibiting fatter tails than public equities.

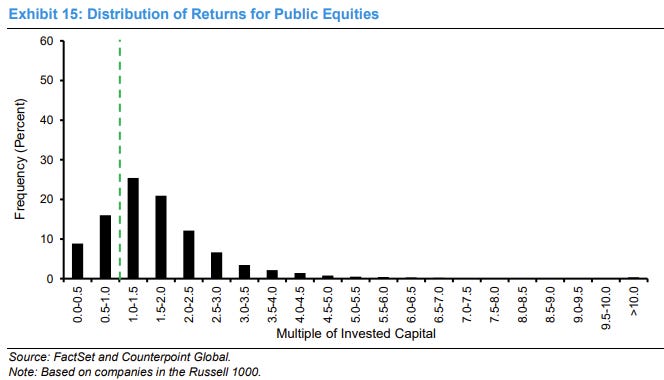

The analysis includes 34,000 observations of 5-year returns, expressed as multiples of invested capital at the beginning of the period, for stocks in the Russell 1000. Data were collected for 35 increments of 5-year returns from year-end 1985 to year-end 2024. Five-year periods were chosen because they align with the historical average holding period for private equity portfolios, with venture capital slightly longer and buyouts slightly shorter. Notably, 25 percent of investments result in losses, the most common outcome is a gain between 1 and 1.5 times the investment, and extreme values are rare.

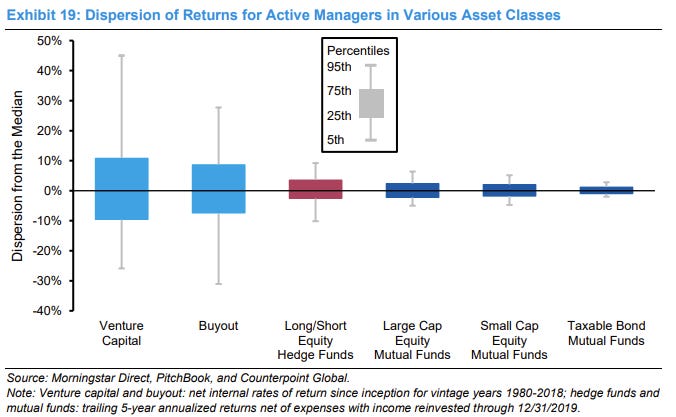

The dispersion of the fund reflects disparities in investment performance across asset classes. Data indicates that venture capital funds exhibit the greatest dispersion, followed by buyout funds, while mutual funds focused on large-cap stocks show significantly lower dispersion. Manager selection matters when it comes to alternatives.

The current state of the stock markets is among the riskiest I’ve witnessed. The extended period without a significant market downturn has fostered a belief that bailouts are inevitable, and that severe bear markets, such as those of 1974, 1987, or 2008, are a thing of the past.

It was also interesting hearing about his mistake with Japanese inflation-linked bonds and his lack of enjoyment in investing.

In the last 45 years, the S&P has posted gains in 34 of those years. The lack of volatility in the past few years makes it hard to believe that the average intra-year decline exceeds 14%.

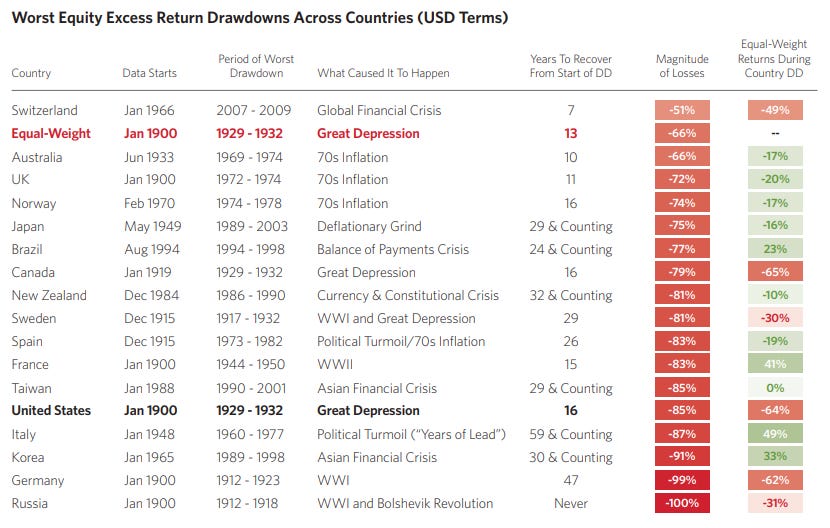

The worst drawdowns for various equity markets around the world. Drawdowns of the magnitude below are very rare but I tend to tell clients and believe, “If it’s happened before, it can happen again.”

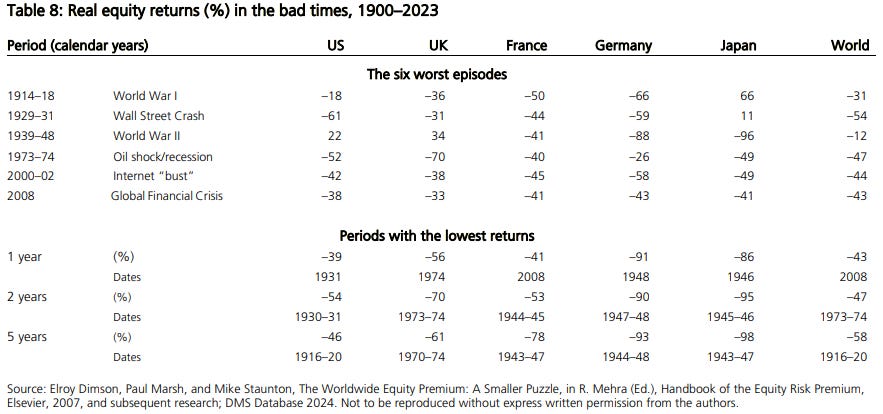

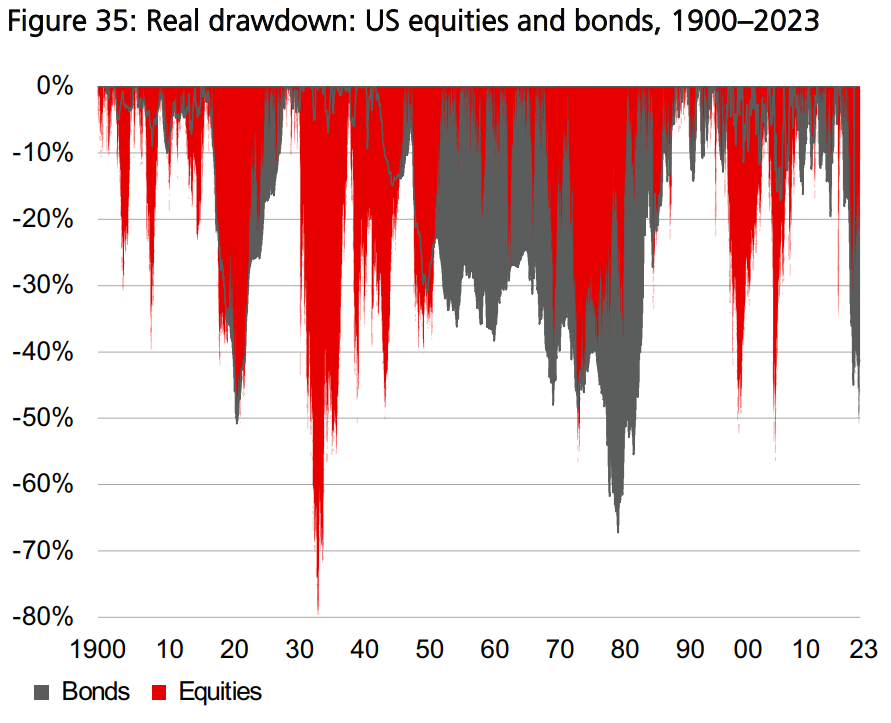

During the worst periods for major equity markets, real returns have been surprisingly poor.

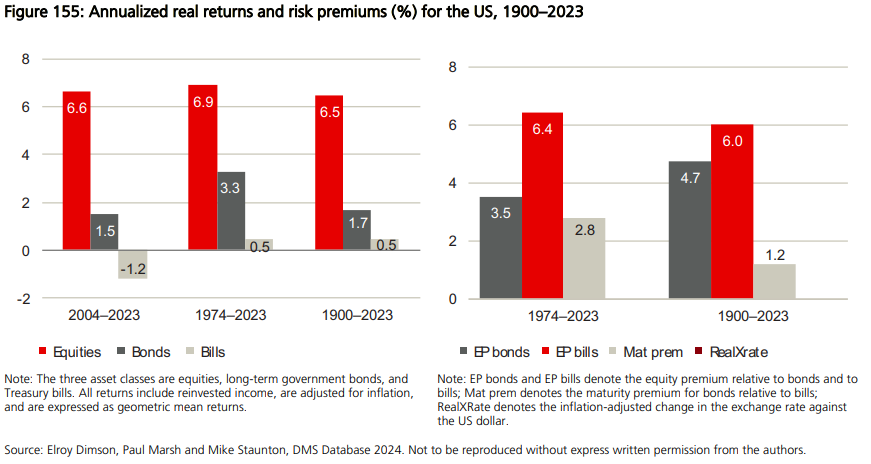

Equities have historically outperformed and delivered strong real returns over the long term, particularly in the US, as shown below. However, poor periods of return tend to occur after periods of extreme valuation.

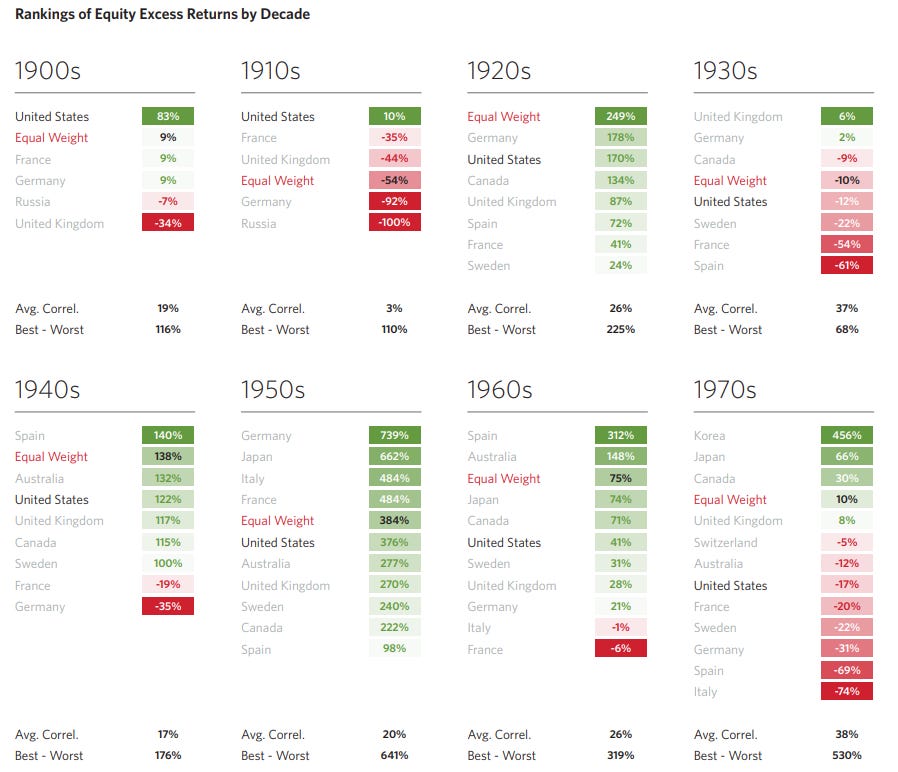

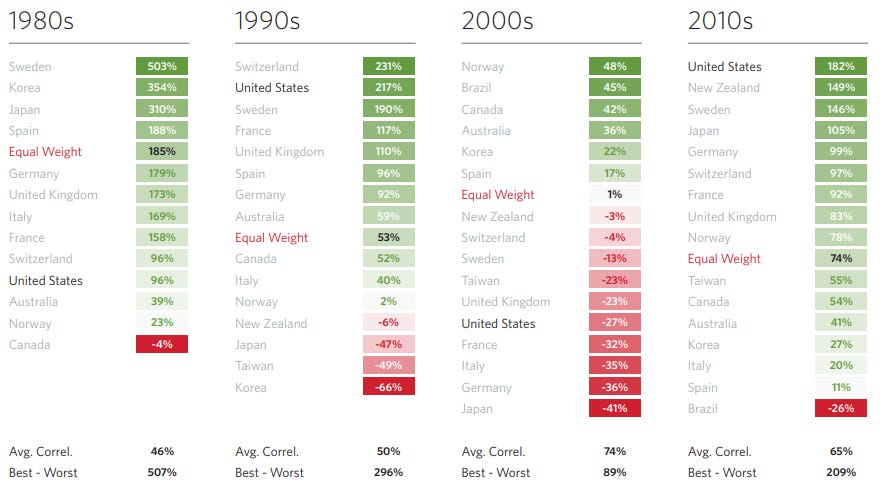

As for US exceptionalism, it probably won’t last. A diversified global approach tends to produce better outcomes. Top geographic equity market performers tend to be fairly random over the decades.

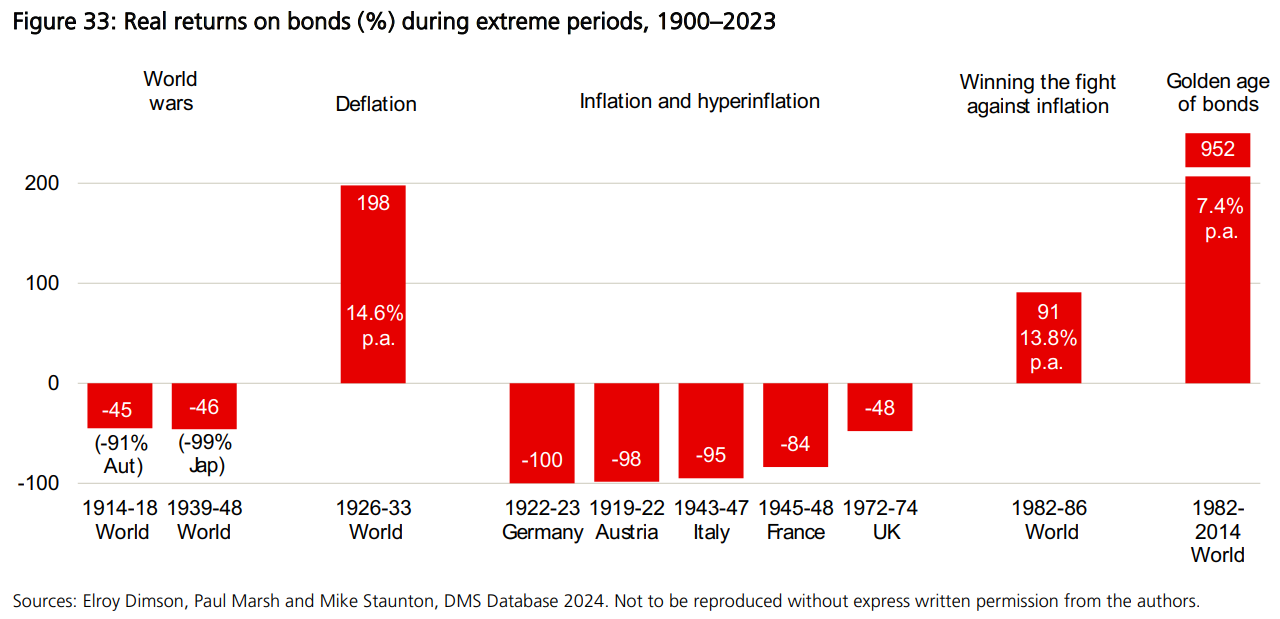

Investors scared by equity market drawdowns may contemplate 100% allocations to bonds. While we have lived through the golden age of bonds, developed world bond markets have faced notable losses as well.

The US bond market has experienced three significant bear periods. The first occurred after a peak in August 1915, leading to a 51% decline in real bond values by June 1920, which remained underwater until August 1927. The second bear market began after a peak in December 1940, resulting in a 67% drop; recovery took from September 1981 to September 1991, marking over 50 years of decline in real terms. The third major drawdown started in July 2020, recording a 51% real loss, making it the second deepest on record. As of late 2023, real bond returns were still 42% below the 2020 peak, with a full recovery expected to take several years.

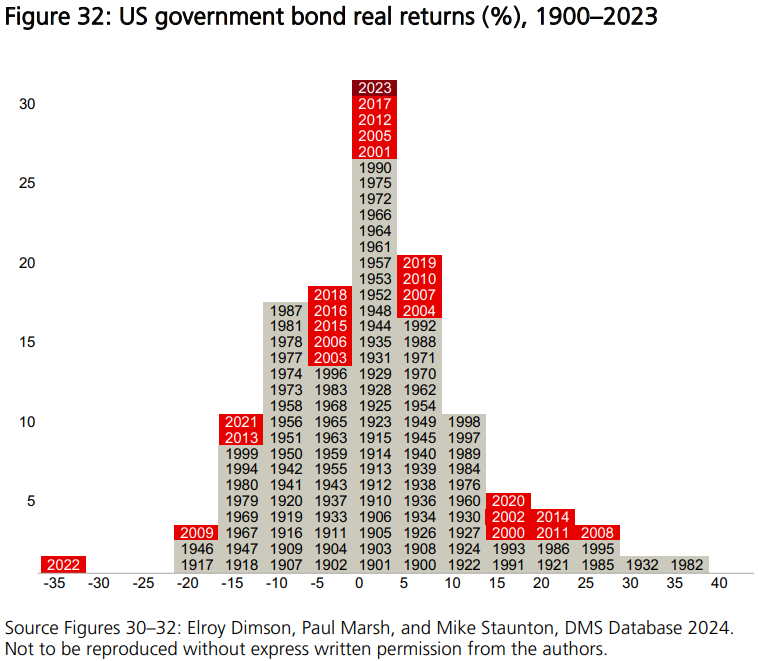

Starting in the late 60s and into the 80s, years with 10-15% real losses weren’t uncommon in the US government bond market.

The key takeaway is that the future is unpredictable, so diversify.