The President the market thought it was getting vs the President the market got (wsj).

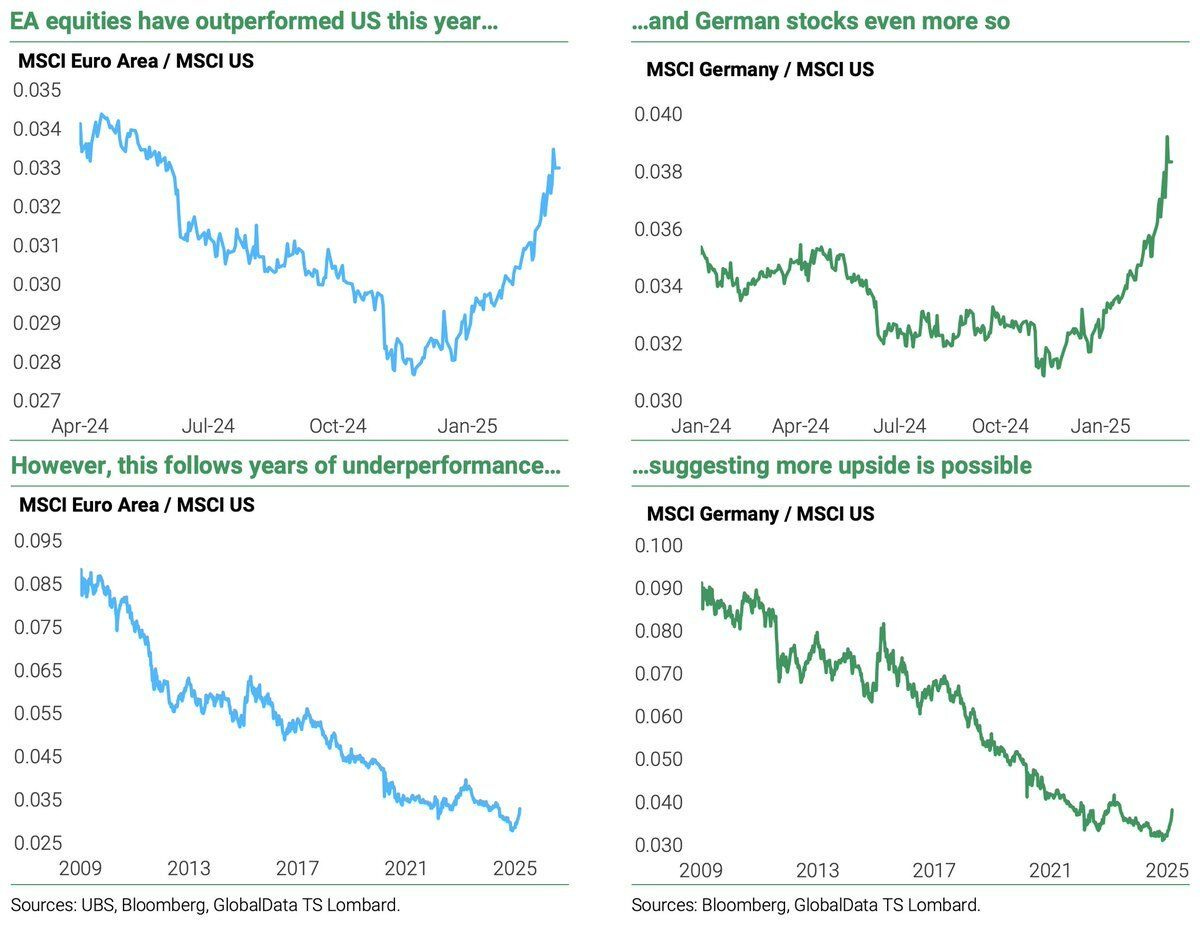

While European stocks have recently outperformed, they have 15 years of underperformance to make up for (TS Lombard via ).

Spoke with a couple from DC who worked in government (one Democrat, one Republican) over the weekend; both expressed serious concerns about US government cuts and were rushing to reducing their DC real estate exposure. DOGE seems to be mirroring Elon’s Twitter slash and burn approach; time will tell if service levels can be maintained with a smaller workforce (Apollo).

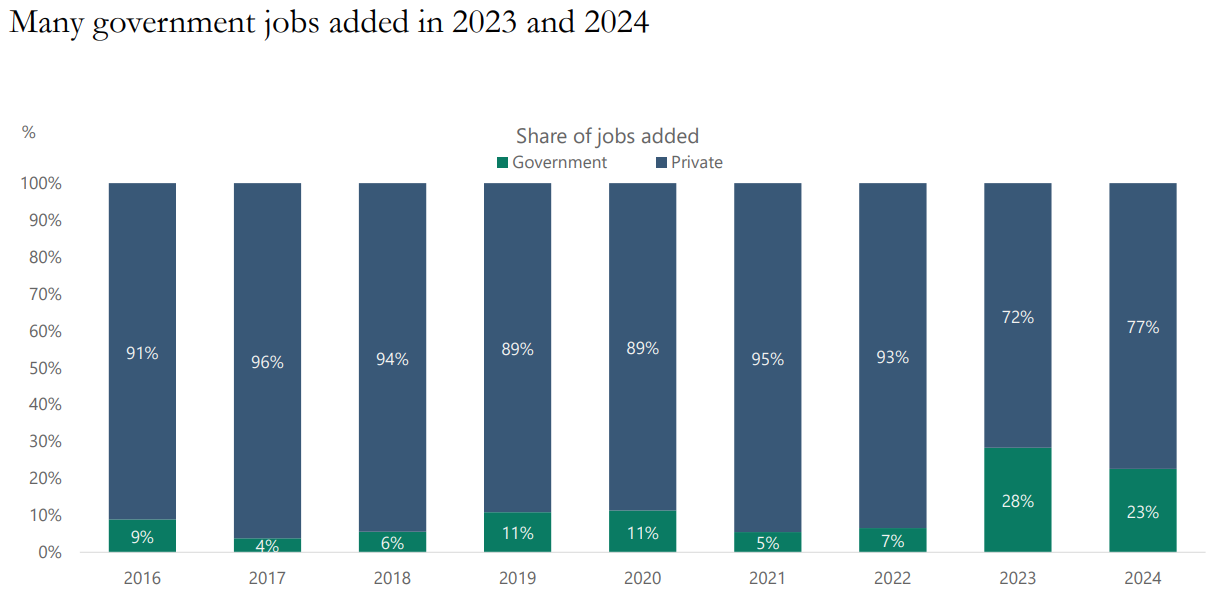

Over the past two years, a disproportionately large share of U.S. job growth has come from government jobs, masking underlying economic weakness (Apollo).

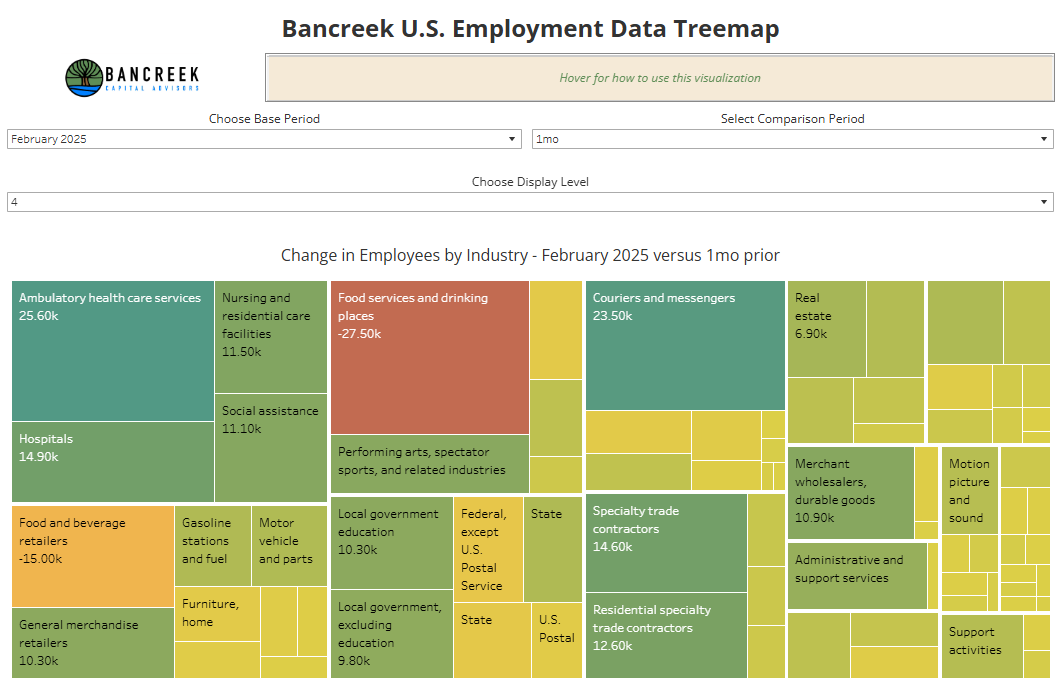

The US economy added 151k jobs in February, 140k of those were private payrolls. No major cuts were visible to government payrolls yet. The additions have been broad based (Bancreek).

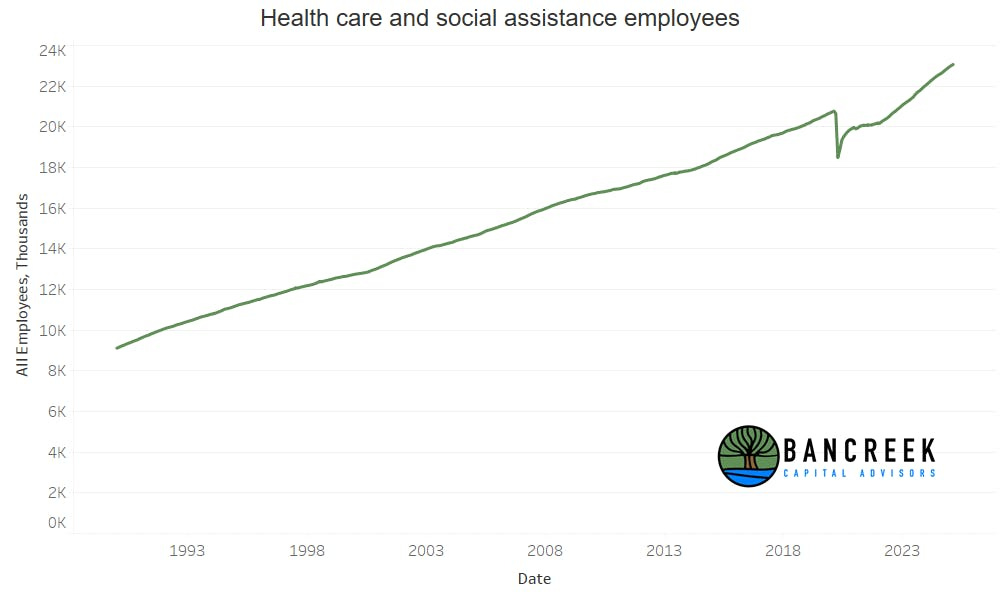

Healthcare has been a major contributor to the US labour market.

This works out to be 62% of the total new private jobs created over the past two years. If we removed these healthcare jobs from the mix, the U.S. has only added, on average, 49k non-healthcare private jobs per month over the past two years – a pretty anemic rate. Tej Parikh from the Financial Times summed this up perfectly in the title of his labor market analysis last year, “America: a healthy or healthcare economy?” The more time has passed, the more it’s looking like it could be the latter.

Consumption in America is dependant on the highest earners. Lower to middle class consumer spending plateaued over a year ago. Will falling asset prices shake the confidence of the top 10% (@BurggrabenH)?

Subprime auto borrowers are falling behind on their payments at a rate higher than the global financial crisis (@barchart).

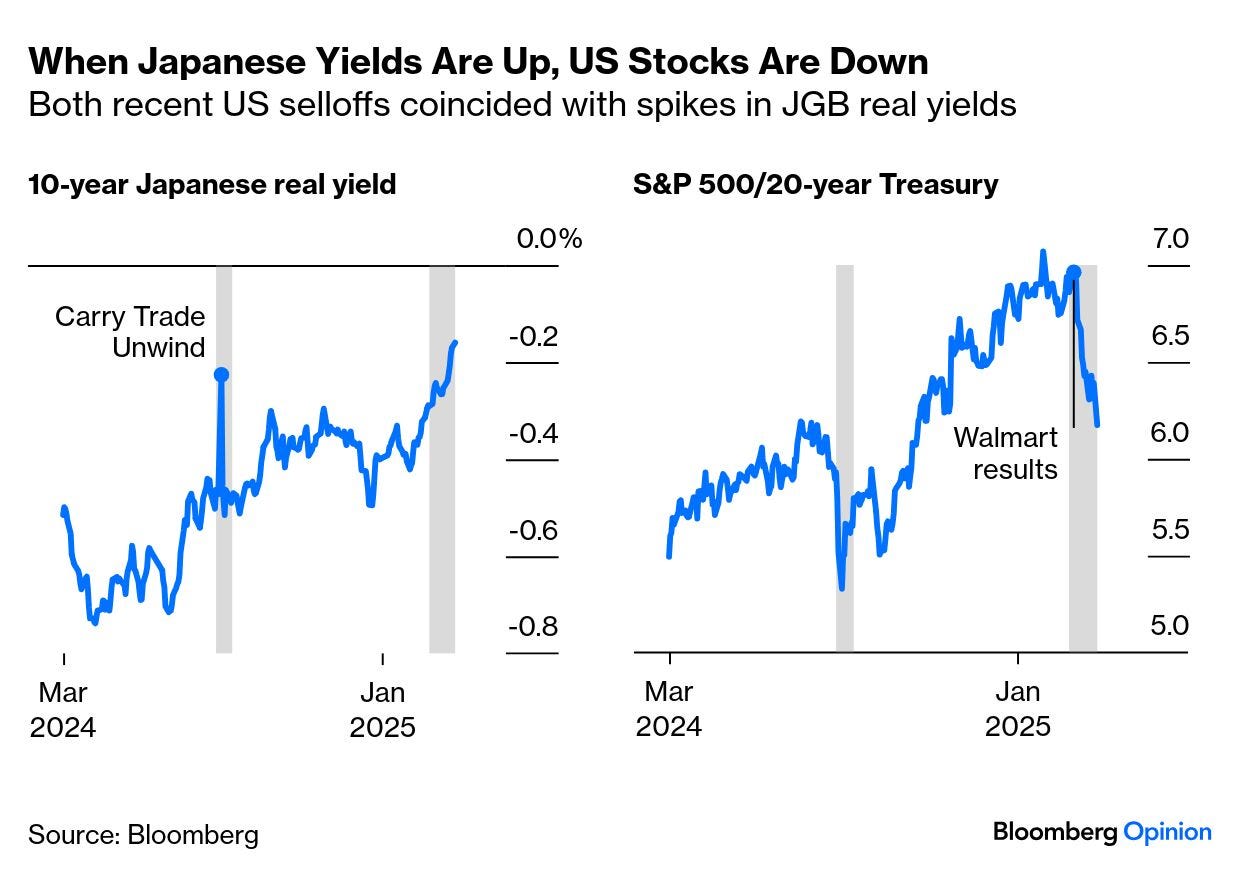

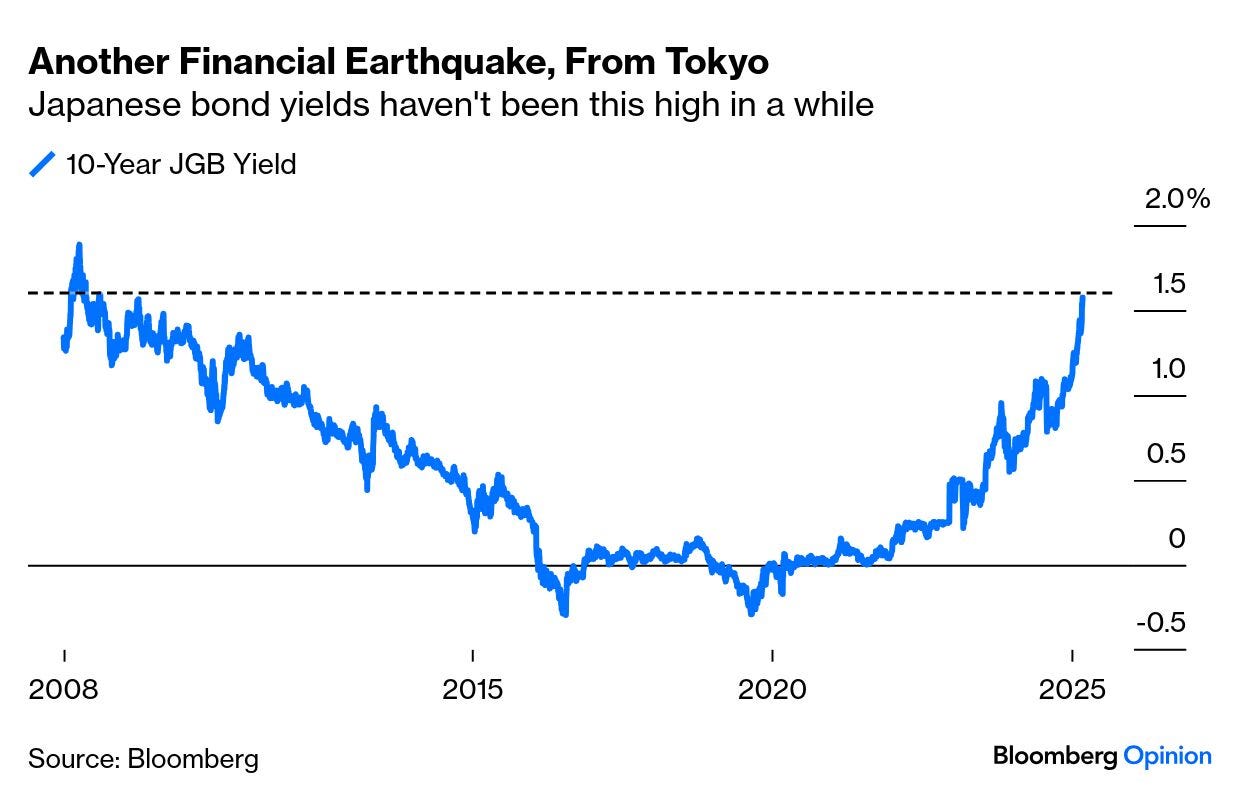

The Japanese 10Y yield has hit levels not seen since 2008 (John Authers).

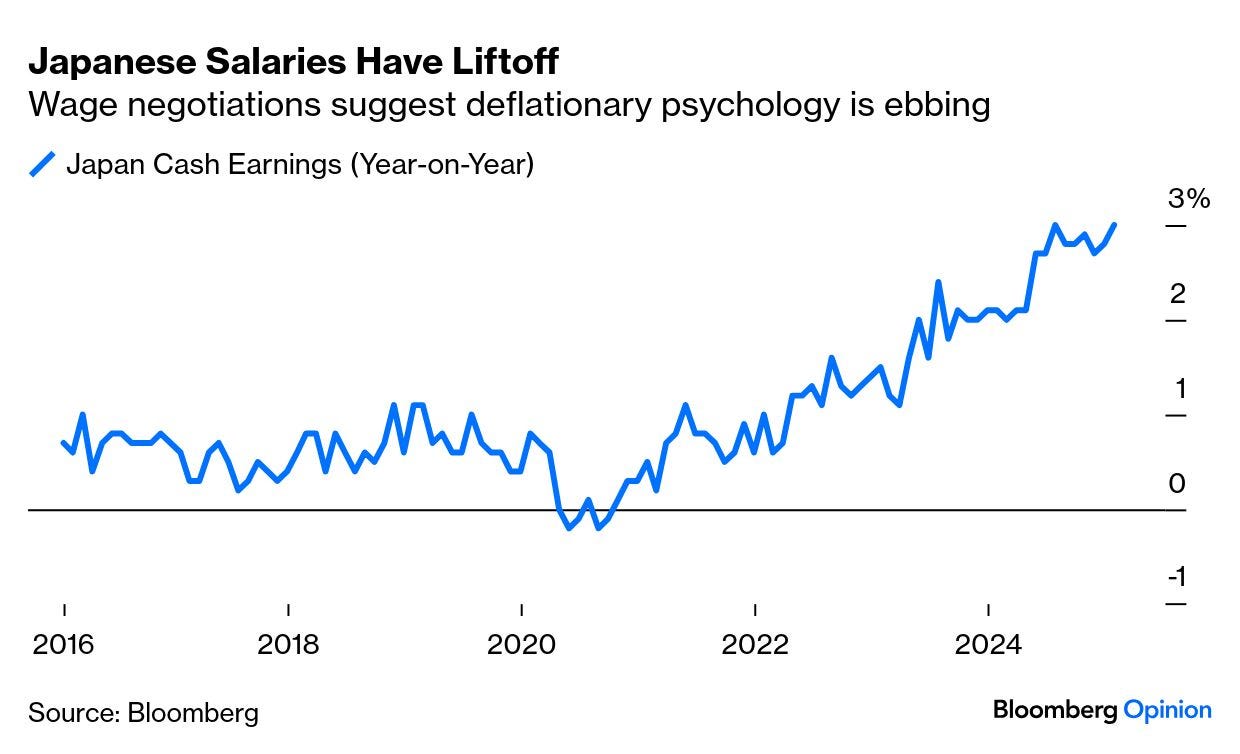

Japanese salaries are beginning to rise after years of stagnation (John Authers).

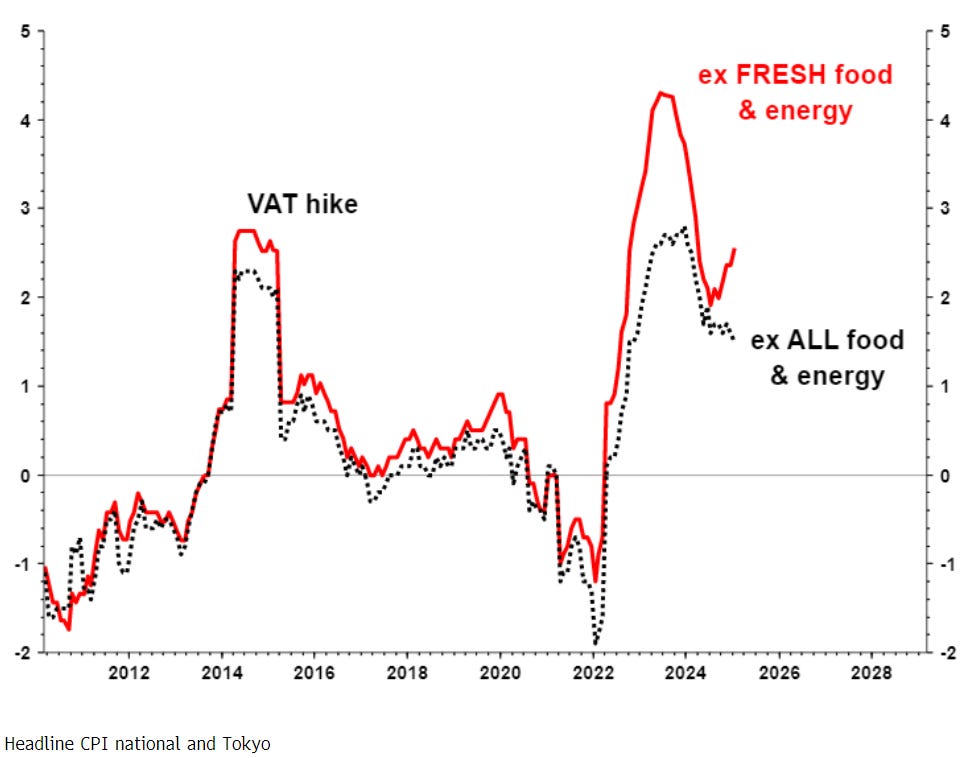

All leading to rising inflation in Japan (John Authers).

Rising Japanese yields are raising concerns about potential cash repatriation to Japan. This repatriation could trigger asset sales, including US stocks, potentially leading to a sell-off as seen during previous yield spikes (John Authers).