Looks like Trump is moving forward with tariffs on Canada and Mexico. The auto manufacturers will be one of the hardest hit industries. Bernstein estimates that the tariffs will add $2700 per vehicle, for an incremental $110 million per day. The dreams of a pro-business administration are fading as uncertainty wrecks havoc.

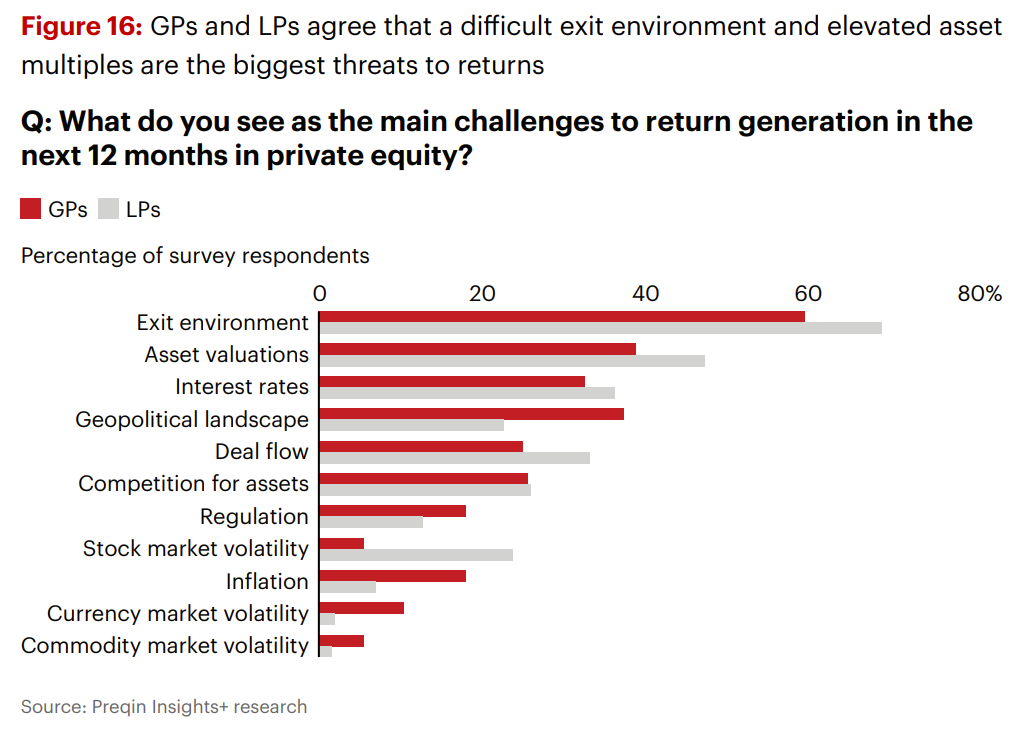

Bain released their 2025 Private Equity report. The exit enviroment remains the number 1 concern for LPs and GPs.

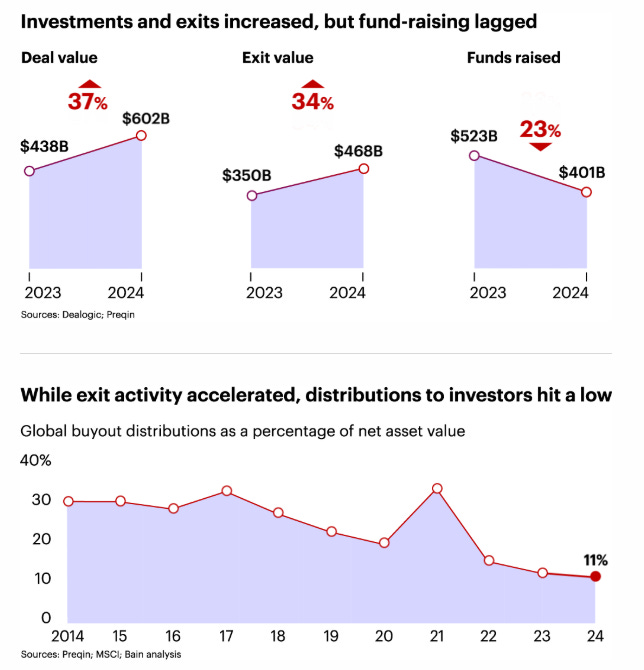

While deal value was up and exits were up, private equity distributions as a percentage of NAV declined further in 2024 to a new decade low.

The J-curve for 2020-22 vintages is one of the worst on record as exit activity relative to assets under management remains subdued.

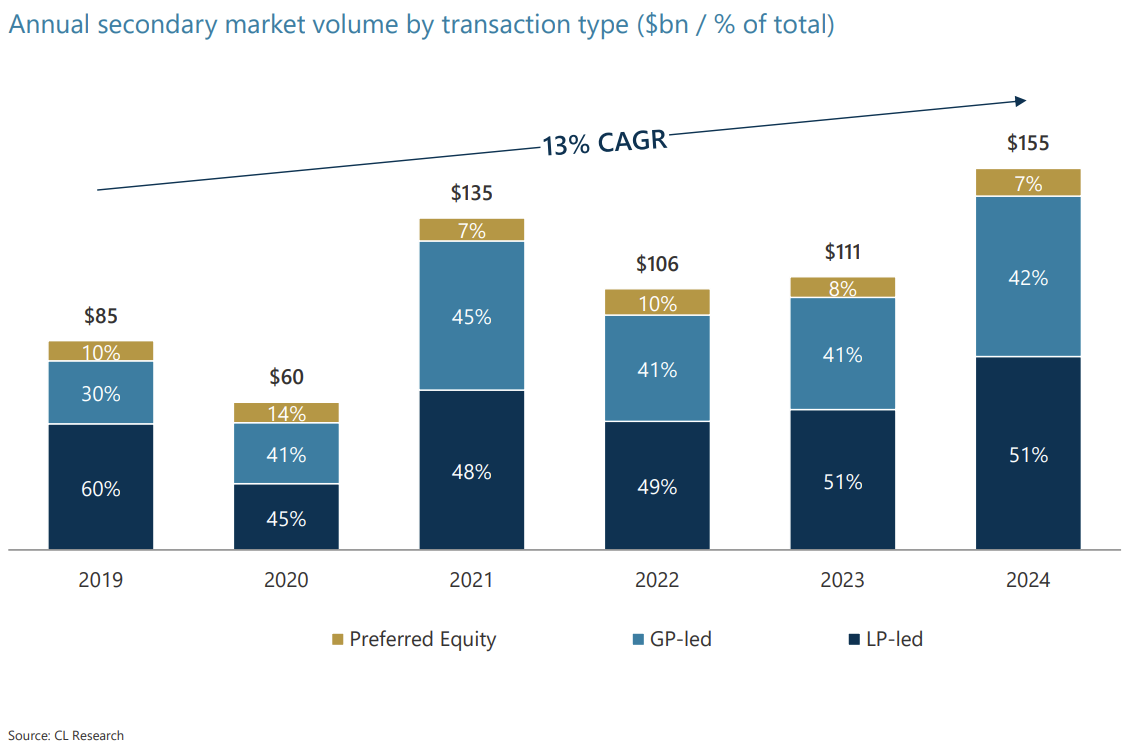

With investors demanding liquidity and other paths to liquidity remaining quite. Secondaries have filled a void. Secondary transaction volume reached its highest level ever at $155 billion; 15% above prior 2021 peak. It’s unclear whether secondary buyers are opportunistically buying trophy assets at a discount or they will be left holding the bag; the answer likely lies somewhere in between.

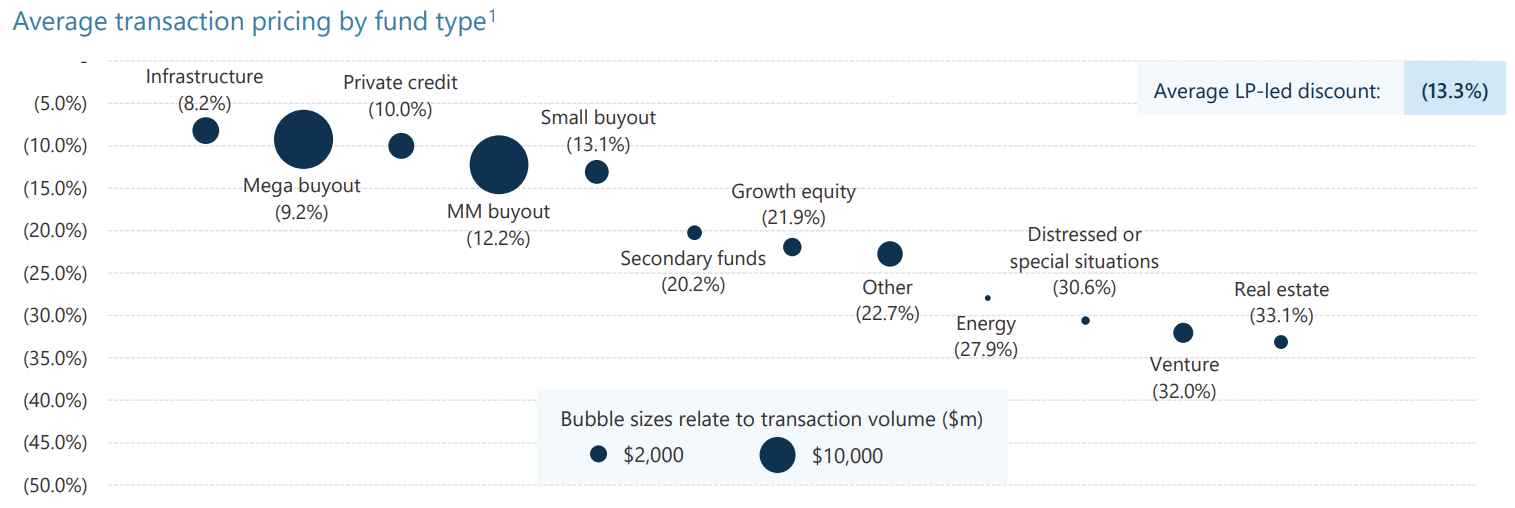

In 2024, average prices for LP-led transactions increased, with quality portfolios trading close to par. Discounts varied significantly depending on the asset class.

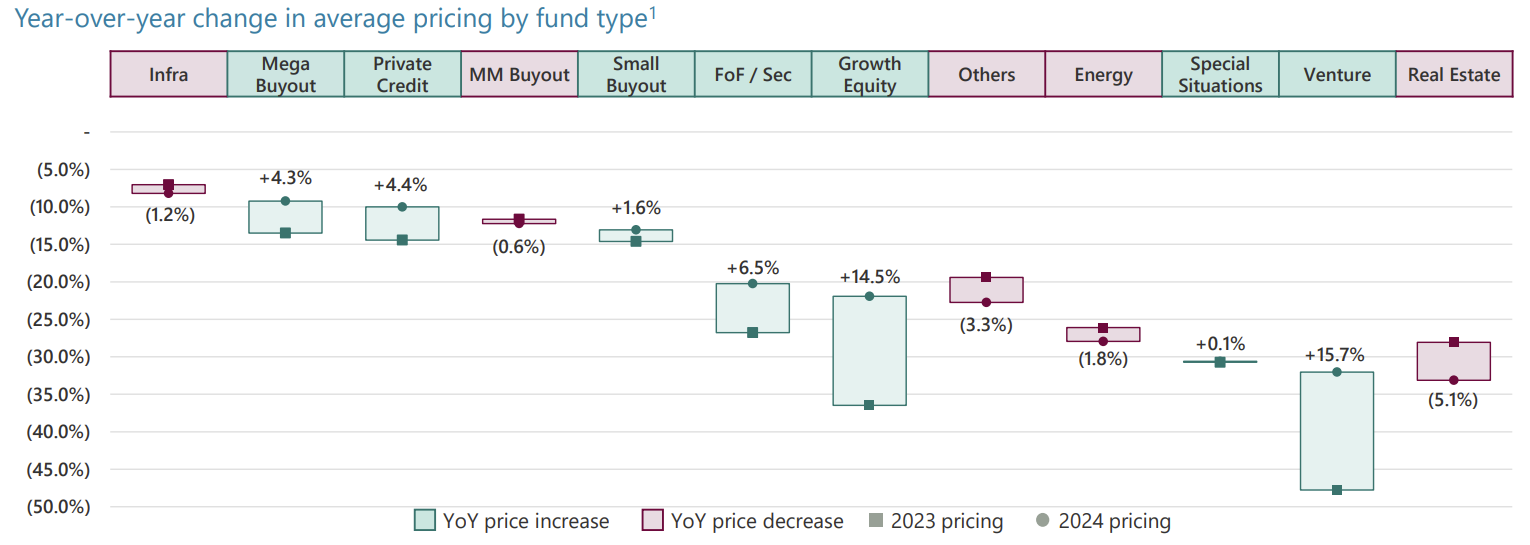

Venture and growth funds showed the most significant pricing improvement in 2024, with average prices increasing by 14-16% compared to 2023.

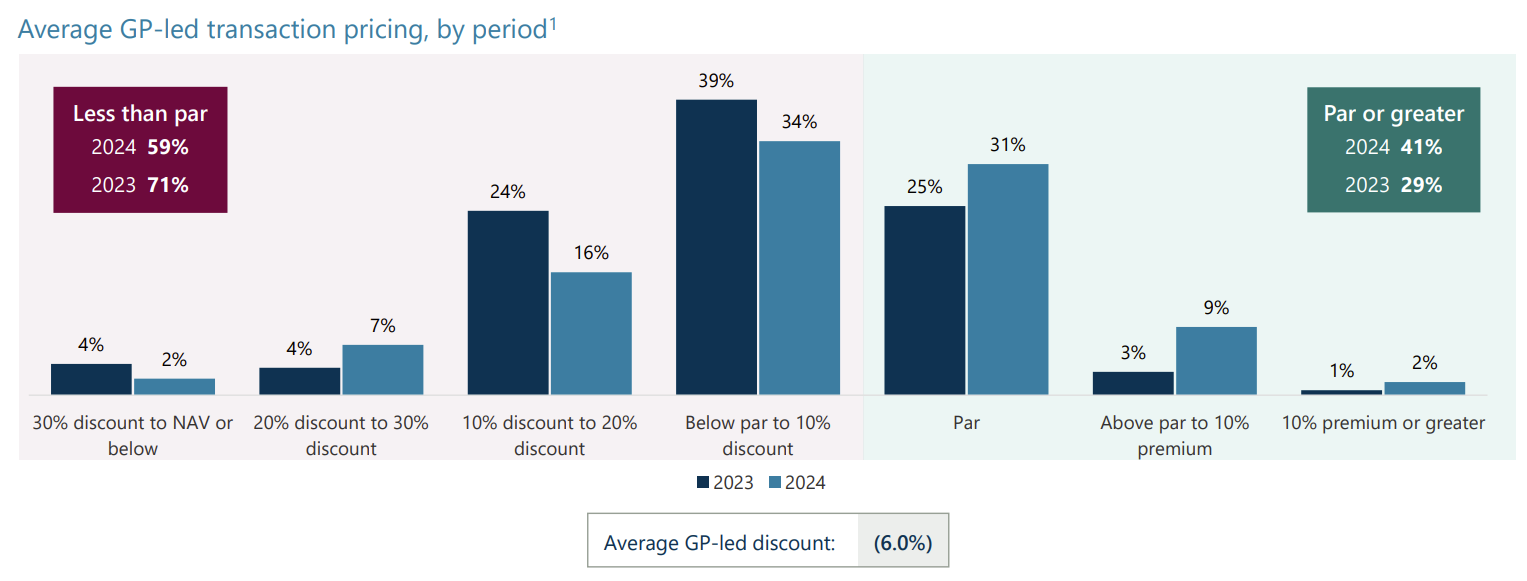

In 2024, 41% of GP led transactions traded above their mark on the books.

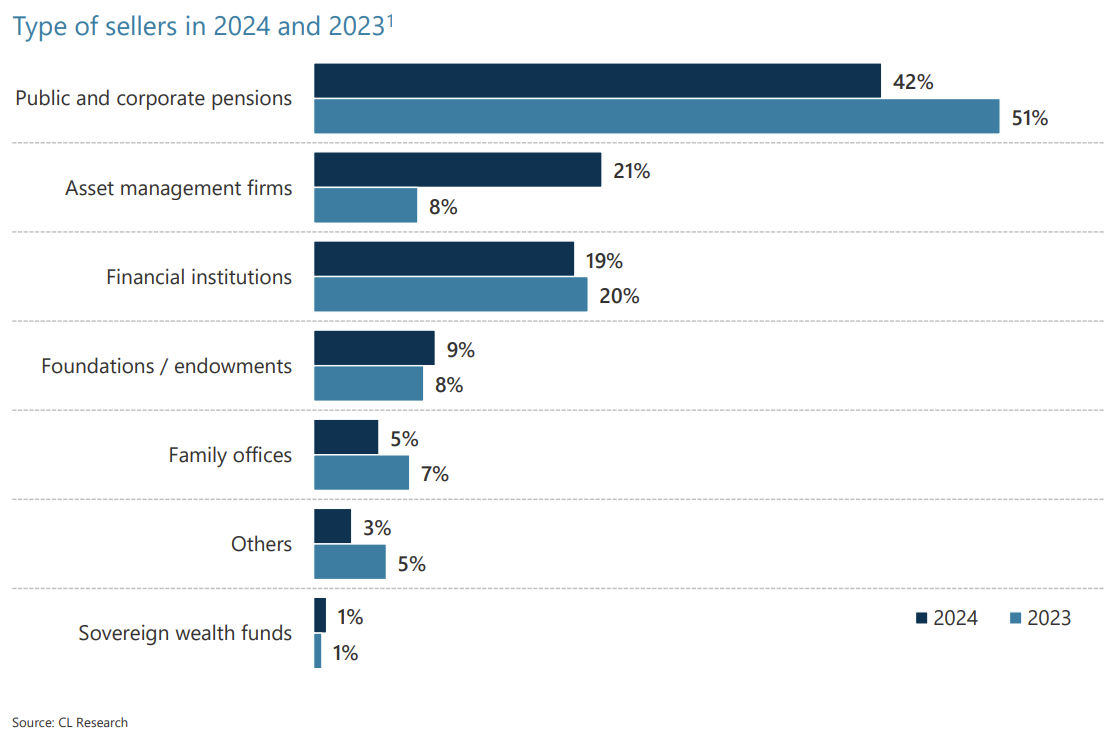

Public and corporate pensions remain the largest sellers; pensions are some of the largest owners of private equity and the principal agent problem drive this, as teams turnover.

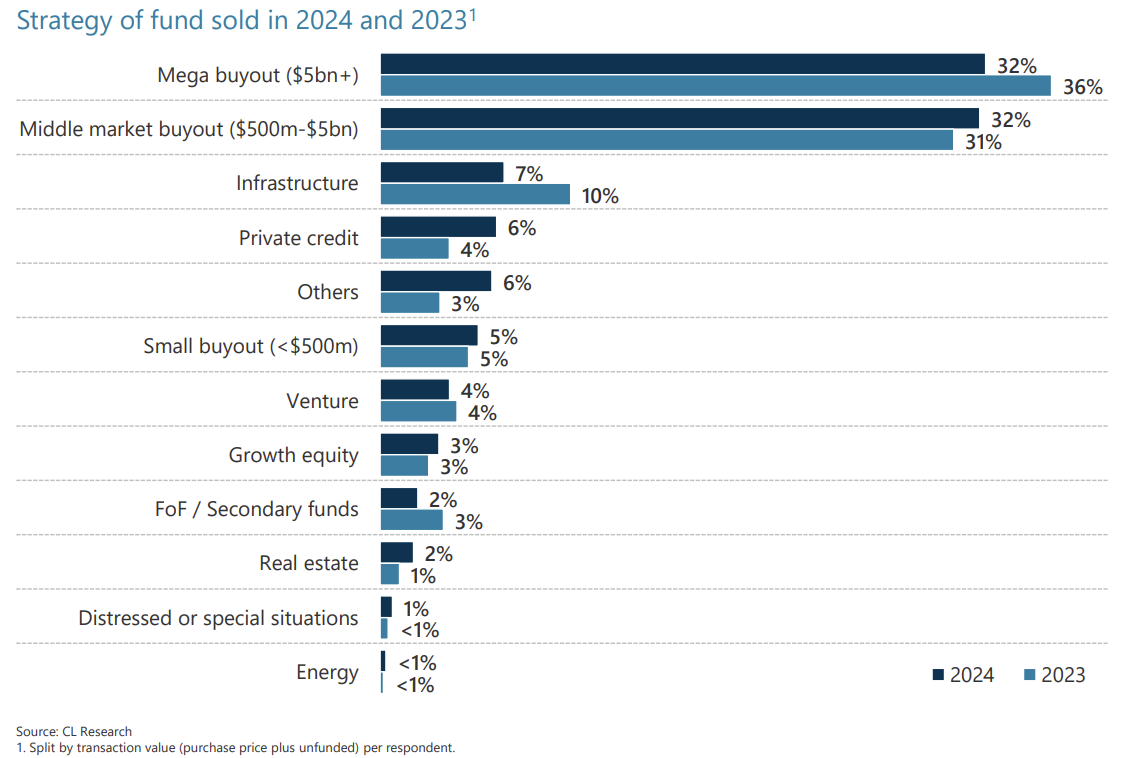

Over 60% of secondary volume are buyout deals.

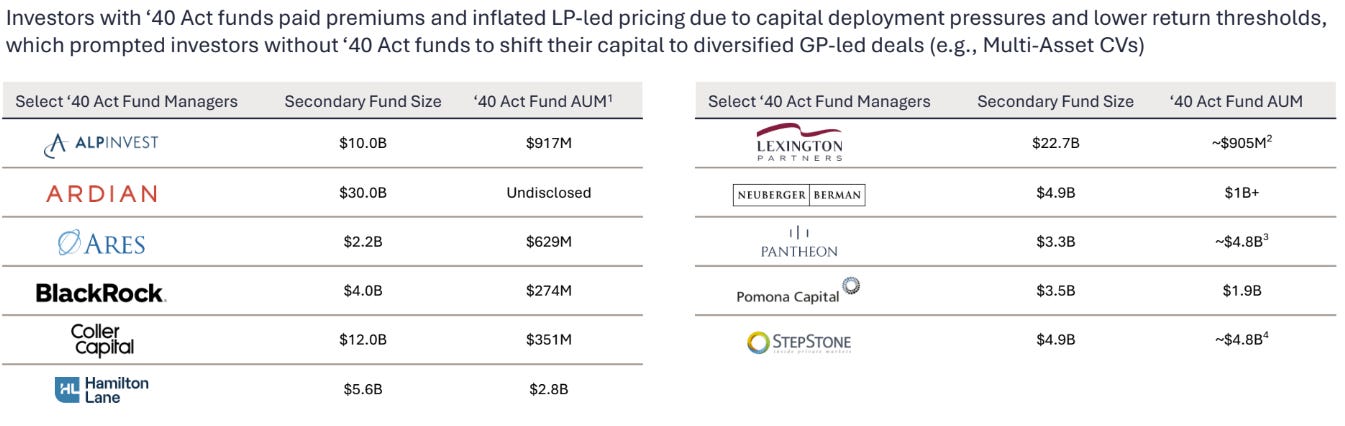

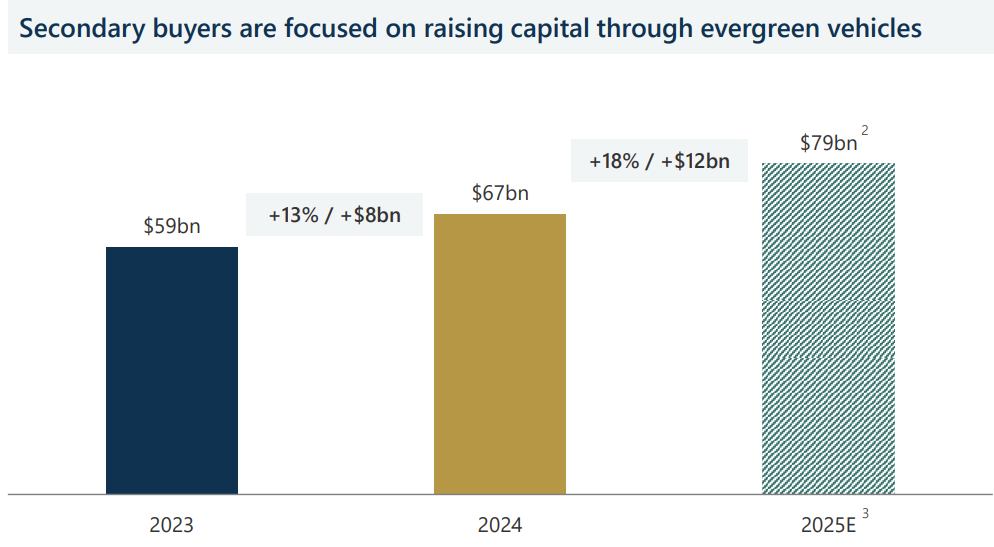

Another trend is the rise of evergreen funds, which had raised almost $70 billion by the end of 2024.

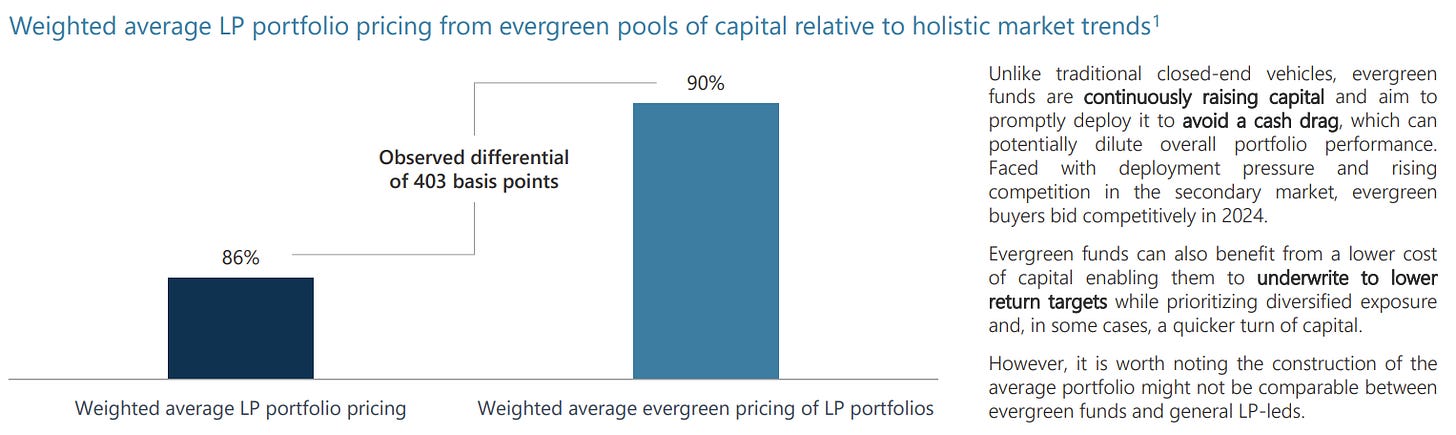

Evergreen funds are changing the market. Evergreen funds want to avoid cash drag and can benefit from a lower cost of capital. Evergreen vehicle transactions outpriced general LP-led transactions by an average of 403 bps in 2024.

The space is dominated by a few behemoths with 4 managers having raised +$10 billion funds.