Even before taking office, the new German government’s massive debt plan is making waves. German bonds suffered their worst day since 1990, with 10-year yields spiking 30 bps.

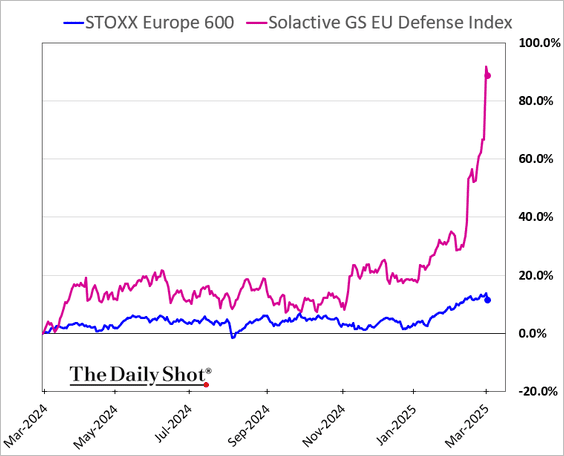

Market is expecting the EU defense sector to be a major beneficiary of stimulus.

The majority of Europeans feel like Ukraine isn’t getting enough support but they don’t want to be the one to actually support!

China is also hopping on the stimulus bandwagon. For 2025, they are targeting the largest deficit in more than 15 years. All roads lead to more spending!

Given the failure of Trump’s initial trade war to curb globalization, the question is whether a renewed approach will yield different results, and if protectionism risks isolating America.

Most Americans are unaware that Canada is their largest foreign oil supplier. I wish the Canadians had shovels in the ground yesterday to begin building the infrastructure to reduce reliance on pipelines through the US.

There’s also speculation that agriculture products may be exempted from tariffs. I guess Trump didn’t realize the US ag industry is dependant on Canadian fertilizer.

Largest importers of fossil fuels from Russia since the beginning of the Ukraine war. Europeans are finding it easier said than done to reduce their dependence on Russian fuels. China and India have benefitted from buying cheap Russian energy.

Cool, AI demo (link). Click in to have a conversation with the future. Call centers are being disrupted.

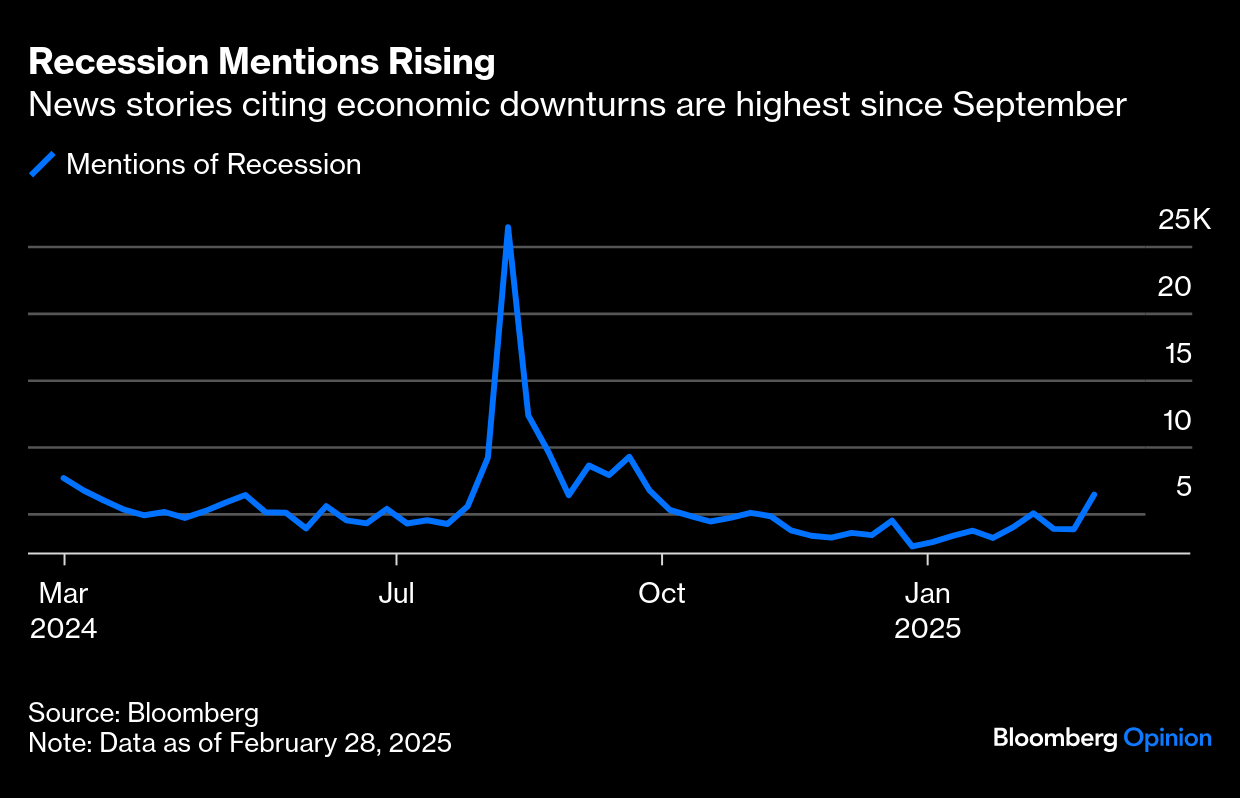

Global trade wars have the market waking up to risks of a policy induced recession.

Investors priced in 2 incremental rate cuts in 2025 over the month of February.

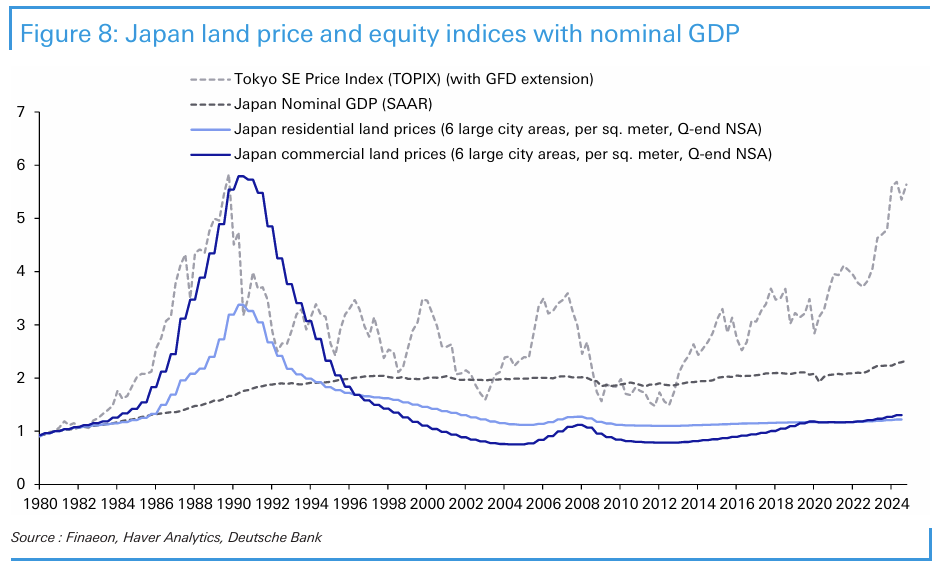

In the late 1980s, Japan faced an unprecedented asset bubble encompassing real estate, stocks, and corporate investment. Fuelled by decades of growth and excess liquidity, Japan’s economy experienced soaring asset values from 1985 to 1989, with stock prices tripling and land prices doubling. By 1990, Japanese real estate value was estimated at four times that of the entire U.S., despite Japan being significantly smaller. At the bubble’s peak, Tokyo’s value equaled that of the entire United States, and the Imperial Palace grounds were purportedly worth more than all of California.

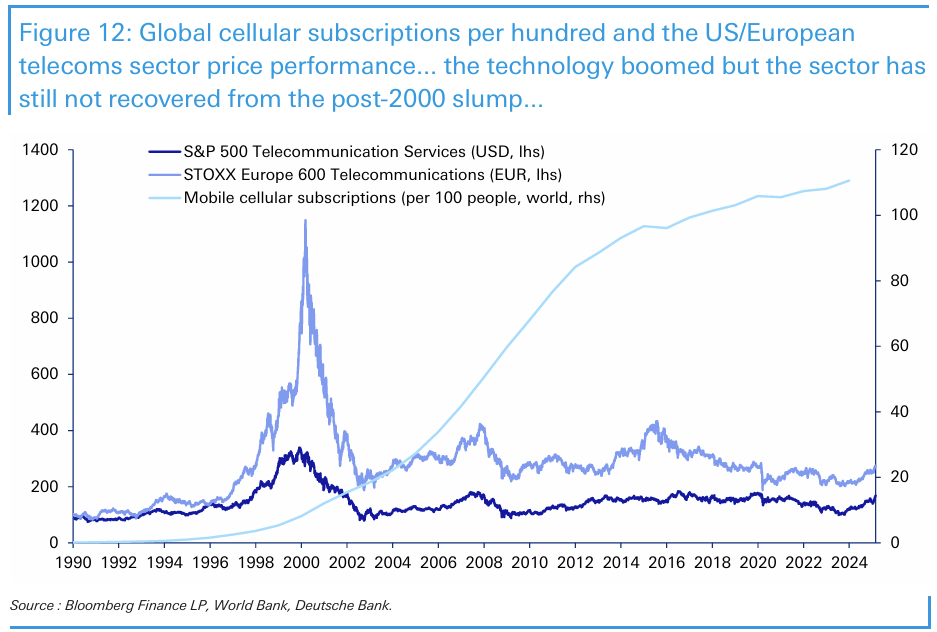

This is a good example of asset prices never or taking decades to reclaim highs.

While 3G rollout in the mid-2000s fueled mobile data growth, it proved a largely destructive bubble for investors. Telecom stocks remain below their 1999 peak, significantly eroding shareholder value, although consumers ultimately benefited.