With the volatility that has tasks of the centerstage with respect to international trade and tariffs, FMCG as an industry, with internal exposure largely (if not completely), it also serves as a defensive game.

And Jyothy Labs has been one of the few superiors of the FMCG stable that returns 233 percent in the last five years, despite the recent correction. It has surpassed the Sector Index, 93 percent of Nifty FMCG returns the doors of the same period and also its peers -Hindusta Unilever (Hul) and Godrej Consumer Products (GCPL), which returned -0.3 percent and 105.6 percent respectively.

Waiting for the growth of profits and profit margins to be moderated, we had recruited investors for partial book profits in July 2024. The action has corrected 38 percent since then; One, due to the deceleration provided for in the growth of the profits and two, the high assessments, while the gain margins have greatly maintained intact.

Quoting at 31 times his profits for fiscal year 26, much closer to the average of five years of 29 times, Jyothy Labs has reasonably corrected its maximum valuation of 50 times in September 2024. It is also a discount at 49 times pairs and GCPL, gains respectively.

Given the favorable risk reward, the stock is a candidate for accumulation at these levels, also backed by other factors listed below.

Segmental dissection

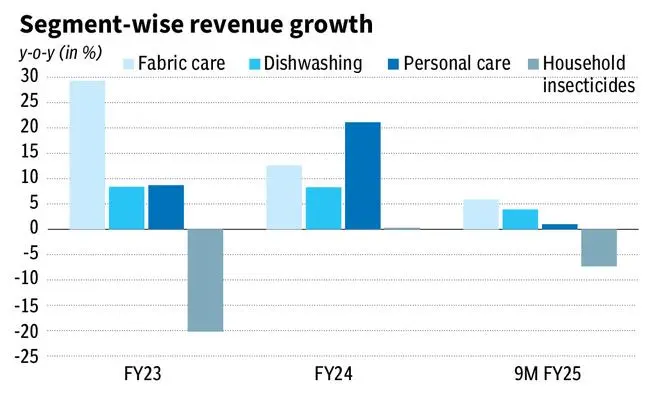

Jyothy Labs is present in four segments: fabric care, dishwasher, domestic insecticides and personal care, with prominent marks such as Ujala, Henko, Exo, Pril, Maxo and Margo.

The care of the fabric continued to be the largest segment (43 percent of the income of the fiscal year24) since the fiscal year22, followed by dishwasher (34 percent), personal care (11.2 percent) and domestic insecticides (7.7 percent).

Fabric Care also has the fastest growing segment with income that grow to a CAG or 20.6 percent of the Fiscal Year 2012-24. While the other segments have grown at high digit half a double digit in the same period, the domestic insecticide segment, however, the duration of the same period and continued to be losses in 9 m fy25.

The year -on -year growth, in all segments, on the other hand, has significantly slowed down in the period of 9 m for fiscal year 2015, in line with industry. In addition, the strong recovery post Covid had to moderate with the base finally catch up. While the domestic insecticide segment continued to drag income growth (-7.3 percent), growth in other segments was in low to alone digits.

Financial metrics

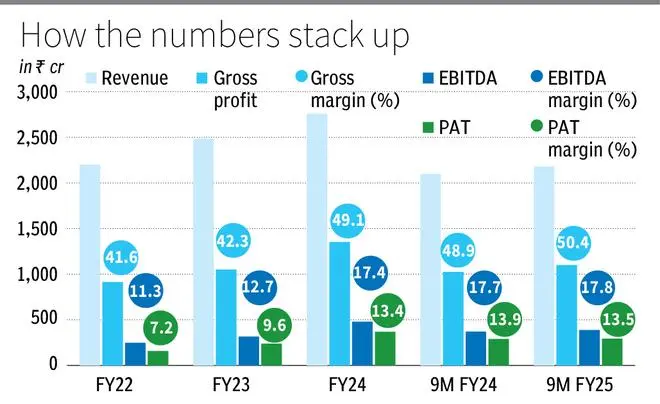

9M The income of fiscal year 2015 constantly grew only 4 percent year after year. But what is more important, this despite a negative price growth of 3 percent, thanks to the growth of the volume.

The gross margins improved the duration of 9 m fy25 to 50.4 percent, an increase of 150 bp, thanks to the prices of the raw materials and the improved combination of products. The benefit also flowed to Ebita, since it increased 4.5 percent, with the Ebitda margin of 10 BPS to 17.8 percent, despite the fact that an increase of 50 BP in employee costs, and the expenses of advertising and sales promotion (A & P), and an increase of 40 BP in other expenses.

The company enjoys a net cash position of the axis of ₹ 659 million rupees or September 2024. The working capital days improved 13 days in the fiscal year 23 to 5 days in the fiscal year24. But he nominally used up to 9 days in H1 Fy25, which is still healthy.

Growth catalysts

Jyothy Labs’s strategy to focus on low units packages (LUPS) has an assistant volume growth. This together with the premiumization and expansion of the portfolio (with new product releases) and the penetration (with new variants of existing products) has been the company’s triple game plan.

Focusing on volume growth, the company transmitted some price benefits for consumers, explaining the negative price growth, while gross margins improved. But the low increase in a single digit in the prices carried out in the personal care segment towards the end of the third quarter followed with some measures to increase wide base prices in the fourth quarter of the Q4 will be an incremental positive, while still prioritizing the growth of the volume.

While the deceleration in urban consumption is expected to maintain volume growth to the single digit digit at least up to H1 Fy26. The rural market, on the other hand, contributing to the rest of 40 percent, has been the savings element. However, the growth of the volume of Jyothy Labs at 7.2 percent for 9 m Fy25 still rises over the growth of 2 percent of Hul and the approximately 4.5 percent GCPL, amid volume trends in decline in the FMCG sector as a whole, said Nielseniq.

In addition, the increase in demand for solid bars to the best margin liquid detergents in the fabric care segment is an important margin growth driver in the medium term. This could accommodate sustained expenses towards sales promotion. A & P expenditure, as a percentage of sales, increased 50 BPS year after year at 9 m for fiscal year 2015 to 8.5 percent. And this also increases from 8.3 percent for fiscal year 200 and 7 percent for fiscal year 23. Management pointed out that A&P spending will be held at these levels to maintain volume growth.

And what is more important, Jyothy Labs is under the segment of care and personal care within the FMCG stable, selling products that are relatively lower on the discretionary scale than the food and drink segment (for example, Nestlé and Britannia). Therefore, it must be isolated relatively better against any sustained deceleration, which is making a good case for accumulation at current levels.

Posted on April 12, 2025